Real Estate

TRREB’s 2026 outlook underestimates growing market risks

The Toronto Regional Real Estate Board’s (TRREB) 2026 market outlook and year in review arrives with an upbeat forecast on sales, but a surprisingly bearish note on prices.

Notably, TRREB engaged MIT researchers to scrutinize Toronto’s new multiplex zoning reform — a standout move that sets a high bar for evidence-based insight. TRREB deserves credit for backing its policy advocacy with serious data analysis.

However, solid research cannot fully mask an outlook that feels too optimistic. A few months ago, even I expected 2026 sales to beat 2025. The thesis just made sense: lower prices and rates mean more affordability, which means more buyers can afford to buy homes.

We actually saw the lowest start to the year for sales on record in TRREB’s Habistat platform. I’ll give TRREB’s team the benefit of the doubt here, though — they likely prepared their forecast long before that data point came out. Now, seeing January’s sales trends, I can’t say I still feel so optimistic. I now suspect 2026 could actually underperform 2025. Let’s get into TRREB’s forecast and try to understand why.

Worsening macro conditions, escalating trade tensions and an early-year sales slump (about 20 per cent fewer transactions than a year ago) have shifted my stance. There are too many headwinds — from rising delinquencies to a cooling job market — to justify unbridled optimism. Let’s acknowledge what TRREB got right, then explore where my view diverges.

Multiplex research: TRREB raises the bar

One thing that really excited me about this report was TRREB’s research on multiplexes. As someone who has been passionately leading the charge in the multiplex space in Canada, this topic is important to me, and I love seeing more resources invested in it.

TRREB’s partnership with MIT to analyze multiplex zoning impacts is a bright spot. Last year, Toronto upzoned citywide to allow duplexes, triplexes and fourplexes in low-rise neighbourhoods. Rather than speculate, TRREB had MIT experts measure the outcome. The study’s takeaway: any price impact from the multiplex reform has been minor, overwhelmed by larger market forces. In other words, allowing more units per lot hasn’t yet caused a significant jump in land values. There may be a slight premium on lots with multiplex potential, but on the order of a few per cent — trivial amid interest rate swings and overall market volatility.

This data-driven insight reminds us that:

• Policy changes need time and favourable conditions to show results; and

• Sometimes, bullish catalysts cannot outweigh negative economic headwinds.

The multiplex reform is a smart long-term move to expand housing options, but the MIT research confirms it is no quick fix in the current market. By investing in such analysis, TRREB has set a higher standard for industry forecasts — backing up assertions with evidence. (I’ll be exploring Toronto’s multiplex trend in depth in an upcoming special report, as this topic merits its own discussion.)

If you’re looking to learn more about multiplexing, we host an annual event in Toronto that brings together some of the brightest minds in the space. Super early-bird tickets are on sale now to REM readers.

A bullish forecast meets reality

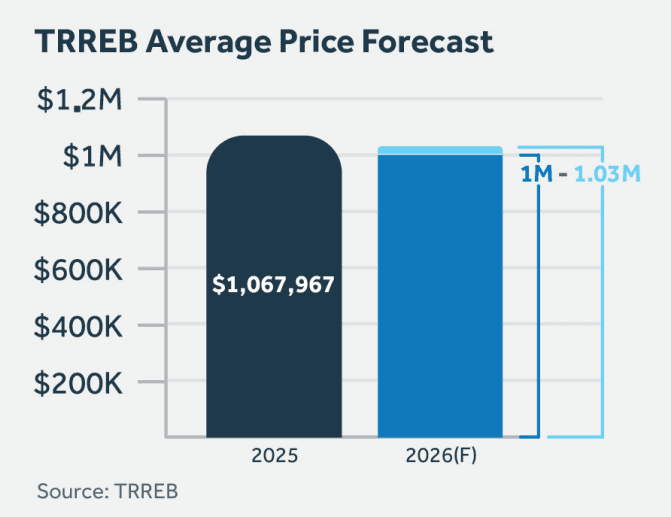

After the MIT deep dive, TRREB’s main market forecast for 2026 strikes a confident tone. The board predicts GTA home sales will hold in the 60,000 to 70,000 range, roughly flat with recent years. It expects the average selling price to land around $1.0 million to $1.03 million, essentially unchanged year over year. The report notes that “year-over-year declines in the mid-to-high single digits will be the norm in the first half of the year.”

In short, TRREB envisions a continuation of the long, slow grind we’ve seen over the past few years — no big crash, but no big rebound. It foresees a stable market that could even see a late-year uptick if consumer confidence improves.

There’s nothing wrong with hoping for stability. After the roller coaster of 2020 to 2022, a calm year would be welcome. But the justification for this upbeat outlook rests on some shaky assumptions. The report suggests pent-up demand will emerge in the second half of 2026, assuming economic conditions improve. It points to better affordability and high immigration as support, noting that 22 per cent of households surveyed intend to buy in 2026, down from 27 per cent in 2025. TRREB also highlights continued population growth and tight rental markets fuelling housing need.

The trouble is that these positives are mostly long-term or conditional. Even if immigration remains strong, many newcomers eventually want to own — but most rent first in the short term. Yes, first-time buyers are out there, but they face affordability constraints. Even with prices down, qualifying for a mortgage and saving a down payment remain difficult.

Tellingly, TRREB’s poll shows buying intent fell from last year, signalling caution, not an impending surge. The pent-up demand narrative assumes buyers sidelined by high rates will jump in once conditions feel safer. So far, that hasn’t happened. Even late 2025 showed little evidence of it despite a stabilizing rate environment. Why expect 2026 to be different unless macro conditions truly improve? And under what circumstances are we imagining Canada’s economy will be better in 2026 than in 2025?

Crucially, TRREB’s forecast hinges on a big “if.” It only holds if the economy and confidence strengthen later in the year — far from certain. A quick reality check: January 2026 home sales were down 19.3 per cent from January 2025, hardly a sign of demand roaring back. Both sales and listings started the year below last year’s pace. It’s hard to reconcile those facts with an optimistic outlook. Barring a dramatic economic upturn, simply matching 2025’s performance may be challenging, let alone exceeding it.

Storm clouds: Key risks for 2026

Several headwinds are intensifying as we move through 2026.

Household financial strain: High interest rates and economic stress are squeezing homeowners. CMHC recently observed that mortgage delinquencies in Toronto have spiked. Arrears have more than quadrupled from pandemic lows and are projected to keep rising into 2026. Toronto faces the strongest increase in delinquency risk nationwide. Many who bought at ultra-low rates are struggling at renewal, and new buyers face stricter lending tests. TRREB data shows a typical renter household faces a $600-a-month gap between what it can afford and the mortgage payment for a starter home. In short, financial pressures are holding back demand. A market can’t mount a sustained recovery while more owners fall behind on loans and renters can’t qualify to become owners.

Source: Canadian Bankers Association

Source: Canadian Bankers Association

Employment and economic uncertainty: The job market isn’t providing much support. Toronto’s unemployment rate hit about nine per cent in 2025, among the highest of Canada’s major cities. Weak employment — and the anxiety that comes with it — makes people think twice about major purchases. Meanwhile, broader economic uncertainty looms. The upcoming 2026 CUSMA review, for example, raises the spectre of tariff frictions that could impact Ontario’s export industries. If businesses feel unsure, hiring and income growth could falter. It’s hard to imagine a surge of buyers until people feel secure in their jobs and the economic outlook.

Source: Statistics Canada; Valery.ca calculations

Source: Statistics Canada; Valery.ca calculations

Demographics and new supply: Toronto’s long-term housing demand is fuelled by population growth, but in the immediate term that engine is less robust. Canada’s population growth has slowed from its 2022 peak. Notably, Ontario saw a rare population dip in the second quarter of 2025 as some residents left for other regions and immigration temporarily cooled. While that is likely a blip, it shows demand cannot be taken for granted in the short run.

At the same time, a wave of new housing supply is hitting the market. Many condo and housing projects launched during the 2021 boom are completing in 2025 and 2026, adding a record number of units. Nationally, housing starts in 2025 were near record highs, and much of that will become 2026 inventory. This surge in supply gives buyers more choice and eases urgency. Combined with cautious demand, it’s a recipe for a slower, more balanced market. It will take time for the new inventory to be absorbed.

In sum, financial strain, employment risk and a shifting supply-demand balance are all pressing on the market. Toronto’s long-term fundamentals — desirability and limited land — remain intact, but in 2026 they are being muted by the economic cycle.

These factors could be mitigated if a recession materialized, giving the Bank of Canada more room to reduce interest rates and improve buying power for those allegedly “waiting on the sidelines.” However, that idea remains a long shot. Canadian Mortgage Trends reports that banks are forecasting anything but rate decreases.

Some optimism could have emerged from OSFI reforming the mortgage stress test in January. I expected some adjustment after a year of studying a loan-to-income cap, but that didn’t happen. The Office of the Superintendent of Financial Institutions has decided to keep existing stress test requirements and confirmed that loan-to-income limits for uninsured mortgages will remain in effect. While OSFI did not issue new guidance on the qualifying rate, it launched a six-month consultation as part of a broader review.

A prudent outlook for the year

Given these headwinds, my outlook for 2026 is guarded. Rather than the gentle climb in sales volume TRREB hopes for, the year may end up flat or even softer than 2025 — which, keep in mind, was one of the weakest years on record. I don’t say this with joy or vindication as the industry’s infamous permabear. I say it with the same care you should use when advising buyers and sellers in a market like this. It’s about setting realistic expectations.

I wouldn’t be surprised if total home sales finish slightly below last year’s level and average prices remain subdued. I would be surprised to see a meaningful flattening toward the end of the year, though I do expect that in 2027. Any improvement will likely be gradual and contingent on real interest rate relief or a pickup in employment.

For real estate professionals, the priority is realism. Sellers should price competitively and prepare for longer listing times. Buyers should take advantage of negotiating power while remaining mindful of high carrying costs. In short, 2026 will reward those grounded in data and pragmatism. The deal frenzy of the pandemic years is behind us — now it’s about strategy and patience.

On the positive side, the industry is addressing structural issues. TRREB’s report calls for speeding up development approvals and supporting new housing construction. These efforts, alongside zoning reforms such as multiplexing, will help in the long run. But they won’t change the short-term reality that 2026 is a year to navigate carefully.

In conclusion, TRREB’s optimism is appreciated, but a healthy dose of skepticism is wise. The best approach is to hope for the best while planning for a challenging market. By staying honest about the data — as TRREB did with the MIT study — we can guide clients and ourselves through whatever 2026 brings. Toronto’s real estate journey is far from over, but for now, caution and clarity are our allies.

Foch: TRREB’s 2026 outlook underestimates growing market risks

Daniel Foch is the Chief Real Estate Officer at Valery.ca, and Host of Canada’s #1 real estate podcast. As co-founder of The Habistat, the onboard data science platform for TRREB & Proptx, he helped the real estate industry to become more transparent, using real-time housing market data to inform decision making for key stakeholders. With over 15 years of experience in the real estate industry, Daniel has advised a broad spectrum of real estate market participants, from 3 levels of government to some of Canada’s largest developers.

Daniel is a trusted voice in the Canadian real estate market, regularly contributing to media outlets such as The Wall Street Journal, CBC, Bloomberg, and The Globe and Mail. His expertise and balanced insights have earned him a dedicated audience of over 100,000 real estate investors across multiple social media platforms, where he shares primary research and market analysis.

ECB and Bank of England to Stand Pat as Iran Conflict Upends Forecasts

2 dead after 4 rescued from Ottawa high-rise apartment unit on fire: officials – Ottawa

Bitcoin Battles Macro Nerves and $75K Sellers This Week

Bob Vylan Banned From U.S. Over Glastonbury Controversy

For five older job seekers, finding new work took creativity, new skills and, in some cases, lowered expectations