Real Estate

Toronto’s housing market is still searching for a bottom

Two months into 2026, the Toronto housing market is showing signs that it may still be working through a correction rather than beginning a recovery.

The latest Market Watch data from the Toronto Regional Real Estate Board (TRREB) shows that 3,868 homes sold in February, down 6.3 per cent compared with February 2025. At first glance, that decline may not seem dramatic. But context matters.

Last year was already one of the weakest years for housing sales in decades. If sales are already tracking below those levels early in 2026, it raises an uncomfortable question: Are we still in the downcycle?

According to my friend Rob Marsiglio, my favourite GTA microeconomic housing analyst, the early data suggests something even more significant may be happening. I’ve included a lot of Rob’s analysis in this month’s report because he’s my go-to when it comes to GTA microeconomics and I’m proud to have him at our brokerage.

The “broken floor” trend

Marsiglio recently pointed out what he calls the “broken floor” trend.

The assumption heading into 2026 was that the market had already reached its bottom in 2025. But February’s numbers suggest that assumption may have been premature.

Instead, 2026 has officially broken the floor established last year, marking the slowest start to a year in more than a decade.

That tells us something important about the current cycle: the typical spring momentum that usually pulls buyers back into the market hasn’t materialized.

Instead, buyers appear to be stuck in a prolonged “wait-and-see” phase.

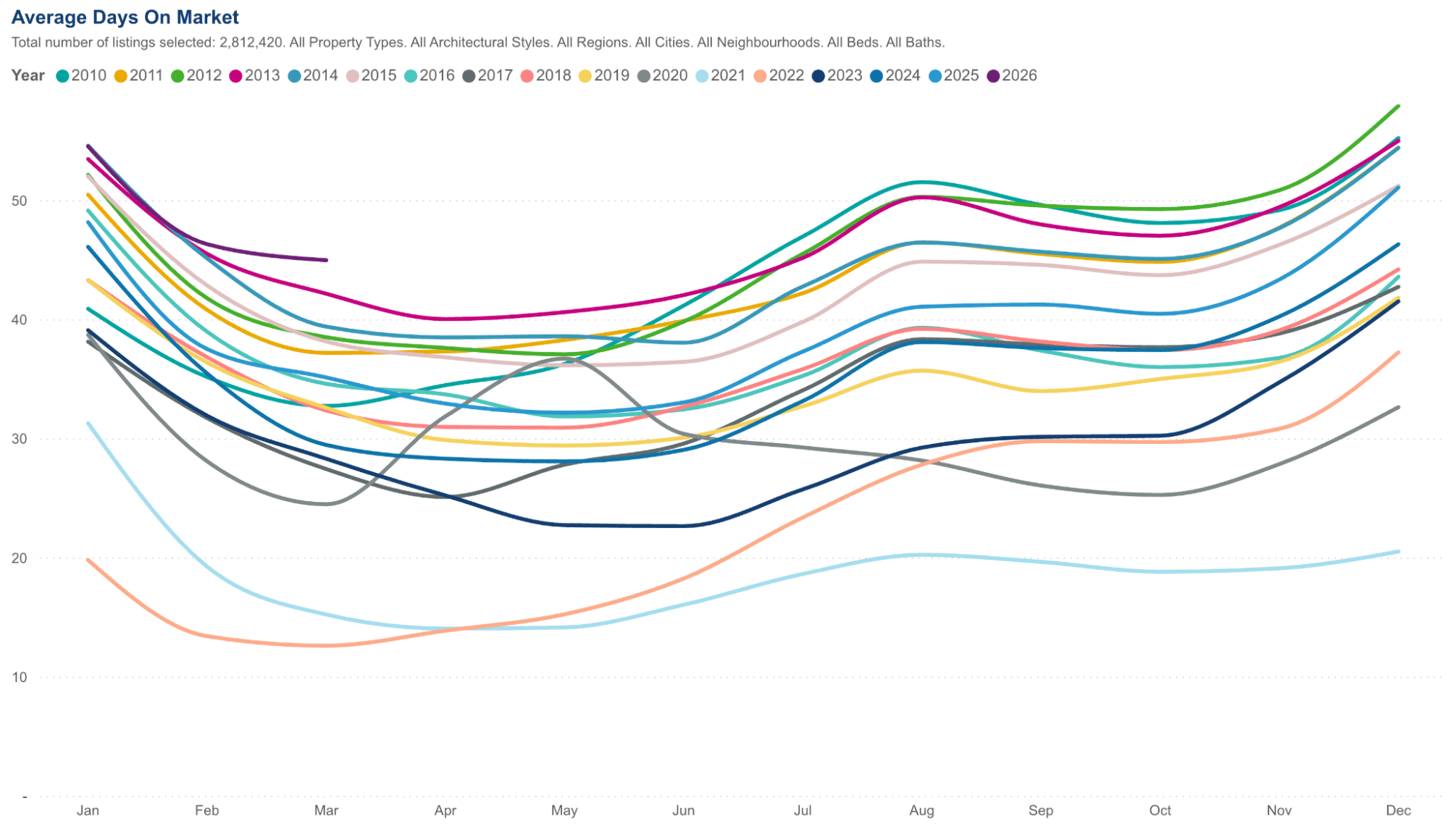

Homes are taking longer to sell

Another clear signal of softer demand is the time it takes to sell a property.

According to the February report:

- Average days on market increased to 36 days, up 33.3 per cent year-over-year.

- Property days on market rose to 54 days, up 28.6 per cent.

When homes start sitting longer, it typically means buyers have more leverage and less urgency.

In other words, the balance of power has shifted.

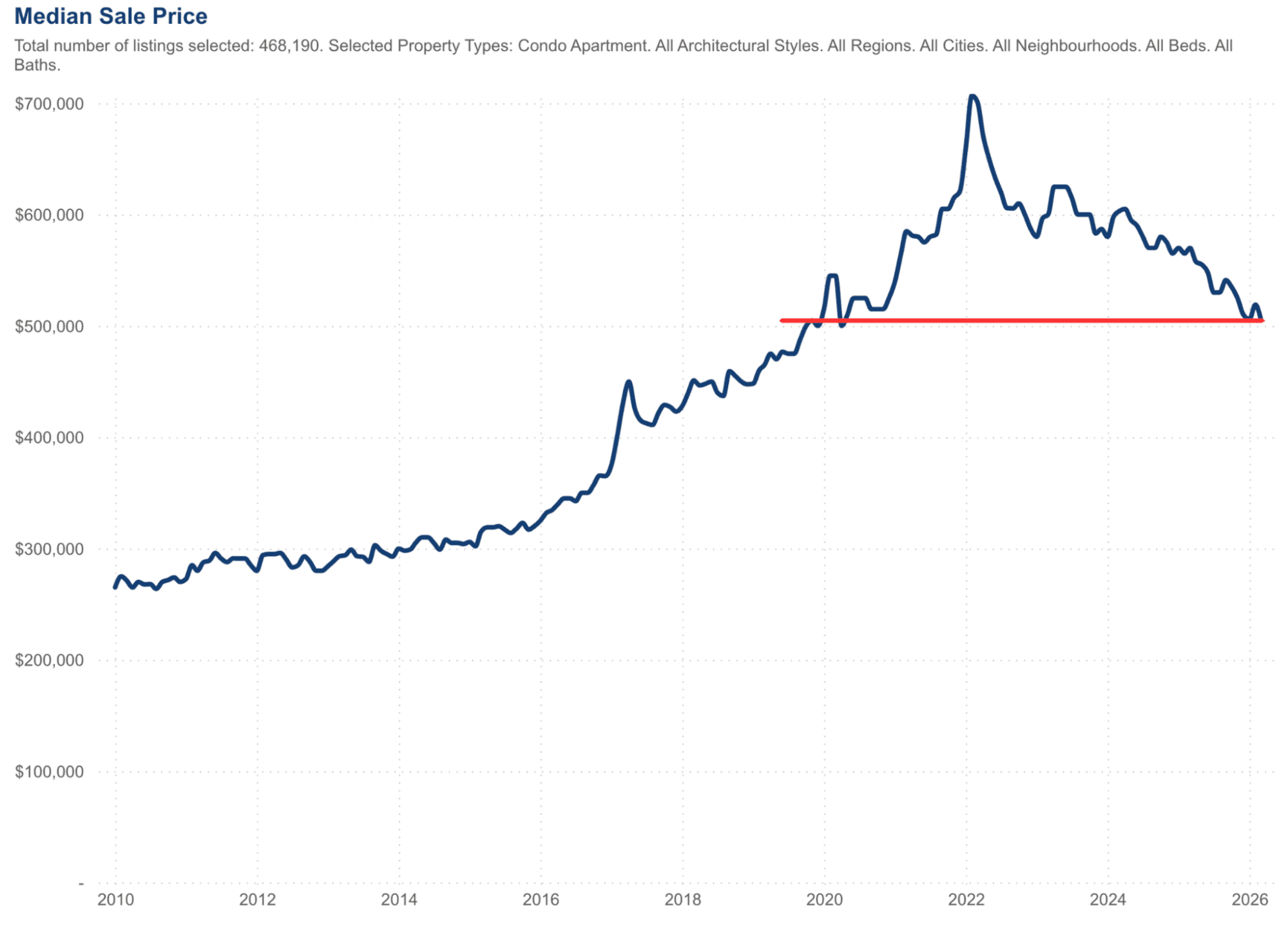

The condo market has come “full circle”

Perhaps the most striking shift is happening in the condominium sector.

Marsiglio notes that median condo prices have now returned to February 2020 levels, roughly $590,000.

That means the condo market has effectively erased six years of appreciation.

While freehold housing still retains some of the price gains from the pandemic era, the entry-level segment of the market has experienced a much more complete recalibration.

This kind of full-cycle reset is historically rare in such a short time period and speaks to the degree of adjustment occurring in Toronto’s housing market.

The inventory paradox

One of the more unusual trends in the February data is what Marsiglio describes as the “inventory paradox.”

Normally, February sees a surge of new listings as sellers prepare for the spring market.

This year, the opposite is happening.

New listings declined 17.7 per cent year-over-year, dropping to 10,705 properties.

At the same time, active inventory also fell slightly, declining about 2.4 per cent year-over-year.

At first glance, declining inventory might suggest strong demand. But that is not what is happening here.

Instead, it appears that sellers are engaging in what Marsiglio calls a “strategic withdrawal.”

Rather than listing their homes into a cooling market, many sellers are choosing to wait.

This creates a kind of stalemate: buyers are waiting for prices to stabilize, while sellers are waiting for conditions to improve.

When both sides pause simultaneously, transaction volumes fall sharply.

A sustained buyer’s market

All of this is pushing the market firmly into buyer’s territory.

Marsiglio points out that months of inventory in the condo market has now exceeded seven months, a level typically associated with clear buyer’s market conditions.

Even the traditionally more resilient freehold segment is showing signs of softening.

For the first time this decade, the sale-price-to-list-price ratio dipped below 100 per cent in February, meaning buyers are successfully negotiating below asking prices on average.

That marks a notable shift from the bidding wars that dominated the market only a few years ago.

Durham Region: The exception

Not every part of the GTA is cooling equally.

One interesting outlier right now is Durham Region, particularly Whitby and Oshawa.

According to Marsiglio’s analysis, Durham currently represents the tightest micro-market in the GTA, with the lowest days on market and sale-price-to-list-price ratios still holding near 100 per cent.

That pattern reinforces a broader trend: relative affordability is now the primary driver of competition.

As lending conditions tighten and borrowing costs remain elevated, buyers are increasingly concentrating in the few remaining freehold markets that still fit within 2026 affordability constraints.

A market still finding its balance

None of this means the market will continue declining indefinitely. Real estate cycles eventually stabilize.

But the early data from 2026 suggests the Toronto housing market has not yet reached a clear turning point.

Sales remain historically weak.

Homes are taking longer to sell.

Prices are still adjusting.

And perhaps most importantly, both buyers and sellers appear to be waiting for clearer signals about where the market is heading.

Until that confidence returns, expectations of a quick rebound may prove optimistic.

For now, the data suggests Toronto’s housing market is still doing what markets often do after a major boom: working its way back toward equilibrium.

Daniel Foch is the Chief Real Estate Officer at Valery.ca, and Host of Canada’s #1 real estate podcast. As co-founder of The Habistat, the onboard data science platform for TRREB & Proptx, he helped the real estate industry to become more transparent, using real-time housing market data to inform decision making for key stakeholders. With over 15 years of experience in the real estate industry, Daniel has advised a broad spectrum of real estate market participants, from 3 levels of government to some of Canada’s largest developers.

Daniel is a trusted voice in the Canadian real estate market, regularly contributing to media outlets such as The Wall Street Journal, CBC, Bloomberg, and The Globe and Mail. His expertise and balanced insights have earned him a dedicated audience of over 100,000 real estate investors across multiple social media platforms, where he shares primary research and market analysis.

Trinidad and Tobago extends state of emergency for 3 months over crime

U.S. politics are getting more polarized and, increasingly, so are state income-tax systems

'The risk is real': Two tigers must be removed from residential property, says mayor of Ontario town

Bob Vylan Banned From U.S. Over Glastonbury Controversy

For five older job seekers, finding new work took creativity, new skills and, in some cases, lowered expectations